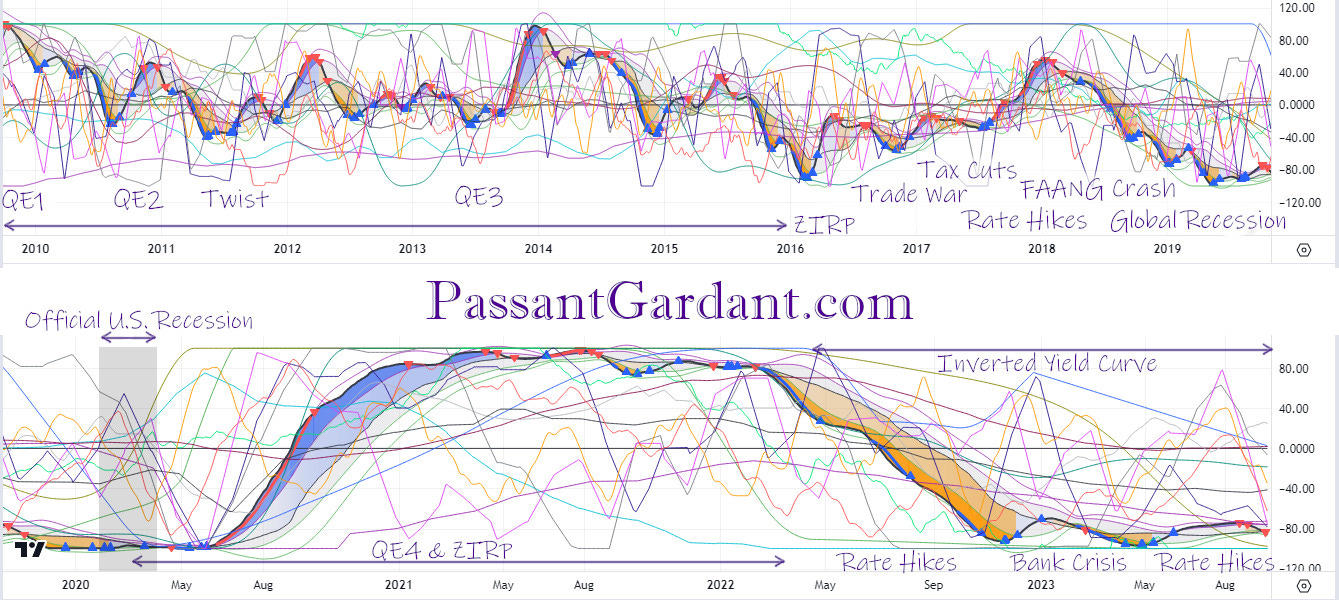

This is my custom Anderson Recession Indicator (ARI) based on 15 economic oscillators. It looks fairly noisy when looking at the individual oscillators, but when taken together, they form a clear and accurate trend and forecast. When the ARI hits -100, that is a recession. When it hits +100, that’s an expansion (or bubble). Nearly the entirety of the 2010s was low growth or contraction with the exception of temporary Fed-policy-induced bubbles which largely evinced themselves in inflated stock market prices. I would go so far as to say that the 2010s was a Depression even though it was technically the longest non-recessionary period ever (although 2016 and 2019 were very near recession). The decade ended at near-recession with clear indication of imminent recession according to the ARI’s 15 oscillators.

The 2020s began of course with a crashing economy, emergency Fed rate cuts, officially-declared U.S. recession, CoViD lockdowns, and monetized stimulus. Between the direct stimulus payments, quantitative easing (QE), zero interest rate policy (ZIRP), and crashing energy prices, an inflationary bubble blew up quickly into 2021. But it also fizzled quickly, peaking in approximately August 2021, and then crashing as the Fed scrambled to fight out-of-control inflation with rate hikes. The yield curve inverted in April and again in June of 2022, and has remained inverted ever since. The stock market sank into bear territory, punctuated by an early 2023 artificial intelligence (AI) bubble, and looks poised to resume it’s downtrend (see my recent This Changes Everything! post). The yield curve environment and liquidity squeeze claimed several banks since March, 2023, and likely many more will fall imminently according to experts and ratings agencies. The ARI in September 2023 looks a lot like it did in December 2019, or worse. All of the oscillators are pointing downward.

Here are the individual components:

[green] United States Money Supply M1, seasonally adjusted — slowing currency supply indicates recession, and this is the first actual contraction in currency supply in about four decades

[olive] velocity of base currency — aggregate currency traded for goods or services (quarterly U.S. GDP x Bureau of Economic Analysis core Personal Consumption Expenditures (PCE) index) divided by the base currency supply — increasing currency velocity indicates a liquidity squeeze which portends recession

[teal] Differential between the Effective Federal Funds Rate (EFFR) and the Taylor Rate, which is a forecasting model used to determine what interest rates should be in order to shift the economy toward stable prices and full employment — the closer the Federal Reserve gets EFFR to the Taylor rate, the less the economy is stimulated, and an unstimulated bubble economy is going to crash

[blue] U.S. Treasury 10-year/2-year yield curve cross indicator — triggers on inversions and reversions, which indicate coming recessions

[lime] U.S. Treasury 10-year/2-year yield curve ratio — flat or inverted is more recessionary versus a steep yield curve when the economy is healthy

[aqua] Bureau of Labor Statistics Consumer Price Index for All Urban Consumers: Energy in U.S. City Average — high energy prices are a leading indicator of recession because energy is an input to everything

[black] Institute for Supply Management (ISM) manufacturing purchasing managers' index (PMI) — under 50 indicates economic contraction

[navy] U.S. consumer credit — falling consumer credit indicates recession

[fuchsia] U.S. durable goods orders excluding defense — slowing durable goods orders indicates recession

[gray] U.S. Census Bureau building permits survey — slowing building permits indicates recession

[silver] Sahm Recession Indicator — three-month moving average of the national U6 unemployment rate relative to its low during the previous 12 months — unemployment is lowest just before a recession

[purple] Deviation of real U.S. gross domestic product (GDP) from the Congressional Budget Office’s (CBO) estimate of the output the economy would produce with a high rate of use of its capital and labor resources — negative output gap indicates recession

[maroon] Differential between Bureau of Labor Statistics Import/Export Price Indices — as import prices rise, standard of living declines; as export prices fall, businesses lose money

[orange] McClellan oscillator — NYSE net stocks advancing/declining percentage — even when some headline-grabbing companies are hitting all-time highs, the economic truth is revealed by how the median company is doing

[red] CBOE put/call ratio — the market gets bearish ahead of recessions due to the aggregate earnings outlooks of all of the companies therein, and so put options exceed call options