Steel, Sovereignty, and the U.S. Dollar

How Government Policies Rusted Out Pennsylvania’s Industrial Powerhouse

Introduction

The decline of Pennsylvania’s steel industry, marked by mill closures and corporate bankruptcies from the 1970s to the early 2000s, is often framed within the context of free trade and comparative advantage – American companies simply outsourced production to countries who had greater natural resources, cheaper labor, a less advanced economy, etc. However, a deeper analysis reveals that political and economic interventions, including the U.S. Dollar’s role as the global reserve currency, were primary drivers, not free-market trade. Established post-World War II and formalized by the Bretton Woods Agreement in 1944, the Dollar’s reserve status required policies prioritizing imports over exports to maintain global Dollar liquidity, benefiting the political and banking classes while exacerbating domestic industrial decline. Fiscal and trade policies bolstered this off-shoring and globalizing trend to favor the interests of the elites over those of the common people and national self-sufficiency.

Historical Context

Pennsylvania Steel

The Pennsylvania steel industry traces its origins to the early 19th century, with the establishment of iron forges and small-scale steel production facilities. By the mid-1800s, advancements in steelmaking technologies, such as the Bessemer process, enabled rapid expansion. Andrew Carnegie’s founding of the Edgar Thomson Steel Works in 1875 near Pittsburgh marked a turning point, laying the foundation for U.S. Steel, the world’s first billion-dollar corporation. Pennsylvania, particularly the Pittsburgh region, became the heart of American steel production, supplying the growing railroad industry, construction projects, and the military with essential materials (Klein, 2001).

Pennsylvania’s rise as a low-cost, high-output steel producer was not accidental—it was deeply rooted in the state’s natural geographic and geological advantages. The region was endowed with abundant raw materials essential for steel production, including high-quality bituminous coal from the Appalachian Basin, vast deposits of iron ore, and limestone for use as a flux in smelting. These resources were often located in close proximity, significantly reducing transportation costs and enabling efficient, large-scale steelmaking operations (Warren, 2001). Additionally, the extensive river systems, especially the Allegheny, Monongahela, and Ohio Rivers, facilitated the inexpensive movement of raw materials and finished products, reinforcing Pennsylvania's logistical advantage.

Beyond its natural resources, Pennsylvania benefited from its strategic location relative to both national and international markets. Situated within a day’s rail journey of major industrial and population centers such as New York, Chicago, and Detroit, the state was ideally positioned to serve the demands of the rapidly industrializing United States. The dense rail networks and the proximity to the Great Lakes and Atlantic ports also enabled efficient export of steel products abroad, particularly during wartime and periods of global infrastructure development. This geographical advantage allowed Pennsylvania producers to achieve economies of scale unmatched by many global competitors (Chandler, 1990).

These factors collectively made Pennsylvania an industrial powerhouse during the 19th and early 20th centuries. Its natural suitability for steel production allowed companies like Carnegie Steel and Bethlehem Steel to thrive, fueling not just regional prosperity but also enabling the United States to project its economic and military power globally. By producing steel at relatively low cost and at unprecedented volumes, Pennsylvania helped lay the material foundation of the modern American economy and its rise to global dominance (Warren, 2001).

Steel from Pennsylvania built the nation’s railways, skyscrapers, bridges, and warships. The state’s mills operated around the clock during both World Wars, contributing to the Allied victories by producing vast quantities of armor, munitions, and naval vessels. The industry also fueled domestic economic growth by creating jobs, attracting immigrant labor, and fostering the rise of industrial cities such as Pittsburgh, Bethlehem, and Harrisburg (Churella, 2012). Pennsylvania's steel industry played an essential role in shaping both the economic and geopolitical power of the United States in the 20th century (Hogan, 1971).

The U.S. Dollar as the Global Reserve Currency

The U.S. Dollar's ascent to global reserve currency status was rooted in post-World War II economic realities. With Europe and Asia devastated, the U.S. emerged as the world’s largest intact industrial power, accounting for 50% of global GDP and holding 75% of global gold reserves (Ghizoni, 2013). The 1944 Bretton Woods Agreement institutionalized this dominance by pegging currencies to the Dollar, which was convertible to gold at $35/ounce (Siripurapu & Berman, 2023). Countries maintained Dollar reserves to stabilize their currencies, while the U.S. guaranteed gold convertibility. This created predictable trade conditions but required strict U.S. fiscal discipline. This system facilitated post-war reconstruction through institutions like the IMF and World Bank, while stabilizing trade via fixed exchange rates (Banquedefrance, n.d.).

Global reserve currency status comes with significant responsibilities and challenges, as highlighted by economist Robert Triffin in his seminal work, Gold and the Dollar Crisis: The Future of Convertibility (1960). Triffin identified a fundamental paradox, now known as the "Triffin dilemma," which states that for a currency to serve as a global reserve, its issuing country must supply the world with sufficient quantities of that currency, typically through trade deficits. Yet, persistent deficits can undermine confidence in the currency, potentially leading to its devaluation and loss of reserve status (Triffin, 1960). This dilemma has shaped U.S. economic policy, often prioritizing global liquidity over domestic industrial health.

Triffin’s analysis was prescient, as by the late 1960s, U.S. spending on the Vietnam War and social programs – "guns and butter" – inflated the currency supply, eroding gold reserves through the arbitrage of exchangeability. Foreign-held dollars surpassed U.S. gold stocks threefold by 1971. President Nixon was forced to sever the Dollar-gold link in 1971 to prevent a run on U.S. gold reserves, effectively ending Bretton Woods. The Smithsonian Agreement (1971) attempted to salvage fixed rates with a devalued dollar, but market pressures forced a shift to floating exchanges by 1973. This caused the Dollar to become a “fiat” currency (Chen, 2024). The Dollar quickly depreciated 7.5% against major currencies and global inflation surged as the gold anchor dissolved.

Despite losing its gold peg, the fiat Dollar’s dominance persisted due to the depth and liquidity of U.S. financial markets, the relative stability of the U.S. economy, the dominance of the U.S. military, special trade agreements with OPEC and Southeast Asian exporters, the Dollar’s continued widespread use in international trade, and a lack of any viable alternative system (Siripurapu & Berman, 2023). The Dollar’s value was not backed by gold but by faith in the U.S. economy and institutions. Despite this shift, the Triffin dilemma persists, as the U.S. continues to run trade deficits to supply the world with dollars to enable global trade, with deficits growing from $53 million in March, 1971, to $162,300 million by March, 2025 (Joint Economic Committee, 2025), undermining that faith in due course.

The Requirement for Trade Deficits: Prioritizing Imports Over Exports

To sustain the Dollar’s reserve status, the U.S. must run persistent trade deficits, ensuring that other countries accumulate dollars for use in international trade, reserves, and investments. This requirement, central to the Triffin dilemma, has led to policies that prioritize imports over exports, often at the expense of domestic industries (Bloomenthal, 2025).

Mechanism of Trade Deficits:

When the U.S. imports more than it exports, it pays for those imports with dollars, which foreign countries then hold as reserves or use for further transactions. This ensures a steady supply of dollars in global markets, maintaining liquidity for international transactions and confidence in the U.S. Dollar (Richter, 2025).

However, as Triffin warned, this reliance on deficits can erode confidence in the Dollar if they become too large or unsustainable, potentially leading to a loss of reserve status (Triffin, 1960). This tension is evident in the U.S.’s chronic trade deficits, which have been financed by foreign holdings of U.S. Treasury securities, allowing low interest rates but making the economy vulnerable to shifts in global confidence.

Policy Implications:

The need for Dollar liquidity has meant tolerating and engendering persistent trade imbalances, with deficits growing significantly over time, absorbing 30 million tons of annual steel imports by 1998 (Eichengreen, 2008). This influx of foreign steel, often produced at artificially low costs due to subsidies and regulations, contributed to the decline of Pennsylvania’s steel industry.

To facilitate trade deficits, the U.S. has pursued free trade agreements and low tariffs, such as those under GATT and later the WTO. These policies have allowed foreign goods, including subsidized steel, to enter the U.S. market, often undercutting domestic producers (U.S. Commerce Department, 1990).

Thus, the structural need for trade deficits, driven by the Dollar’s reserve status, has created an environment where domestic industries like steel face significant challenges, as highlighted by the Triffin dilemma.

Benefits to the Political and Banking Classes

The Dollar’s reserve status has primarily benefited the political and banking elites, reinforcing their power and wealth while disadvantaging the broader population, especially manufacturing workers.

Political Class:

The Dollar’s dominance provides geopolitical leverage, as countries reliant on dollars for trade and reserves often align with U.S. policies to maintain access to global financial systems. For instance, the U.S. can impose effective financial sanctions, as seen in recent actions against Russia and Iran, because many nations must use dollars for international transactions (Lahiri, 2023).

The U.S. government can borrow at lower interest rates due to constant global demand for dollar-denominated assets, such as U.S. Treasury securities. This allows financing of deficits and public spending without the constraints faced by other nations (Chen, 2022).

Economic stability during global uncertainty is another benefit, as foreign demand for dollars and U.S. assets acts as a buffer against shocks, enhancing the political class’s ability to manage domestic policy.

Banking Class:

U.S. banks handle a disproportionate share of global financial transactions, given that most international trade is conducted in dollars, generating significant revenue for Wall Street and other financial institutions (Lahiri, 2023).

The high demand for dollars allows U.S. banks to borrow at lower rates, reducing their cost of capital and increasing profitability (Chen, 2022).

The centrality of the Dollar in global finance gives U.S. banks outsized influence over international economic policies and standards, further enhancing their competitive position.

These benefits, however, come at a cost to domestic industries like steel, which have faced increased competition from foreign imports.

David Ricardo’s Theory of Comparative Advantage and Its Misapplication

Apologists for the politicians and bankers will cite David Ricardo’s theory of comparative advantage, outlined in On the Principles of Political Economy and Taxation (1817), which suggests that nations should specialize in goods they produce at the lowest opportunity cost, trading freely to maximize global efficiency. They say that the United States is simply less efficient at manufacturing steel when imports are so cheap, and so we shouldn’t. However, historical data shows that the cost advantages of foreign steel producers were not natural but artificially created through government interventions, violating Ricardo’s assumptions.

Foreign Interventions:

Japan’s MITI invested $500 million annually in subsidies during the 1950s–1970s, enabling firms like Nippon Steel to build modern basic oxygen furnace (BOF) plants, producing steel at $250–$300 per ton compared to Pennsylvania’s $400–$500 per ton using outdated open-hearth furnaces (80% of U.S. production, 1960) (Hoerr, 1988).

South Korea’s POSCO, funded by $1.2 billion in state loans (1968–1980), produced steel at $200–$250 per ton by 1985, with state-suppressed labor costs ($2–$5 per hour) (OECD, 2006).

When China identified steel as a strategic industry in the early 2000s, its government ramped up steel production with massive subsidies. Total energy subsidies to Chinese steel from 2000 to mid-2007 reached $27.1 billion, producing 800 million tons at $150–$200 per ton by 2010, often below cost due to state support and lax environmental regulations (USITC, 2010).

U.S. Interventions:

Environmental regulations, such as the Clean Air Act (1970), added $20–$50 million per plant in compliance costs, increasing production costs by $20–$50 per ton (Misa, 1995).

Labor costs, with United Steelworkers (USWA) wages at $12 per hour in 1975 and $20–$30 per hour by 2000, added $50–$100 per ton compared to foreign labor costs of $1–$5 per hour (Hoerr, 1988).

The lack of industrial policy meant U.S. steel research and development spending was only $50 million annually, compared to Japan’s $500 million, while high interest rates (15–20%, 1980s) blocked modernization efforts (Tiffany, 1988).

Dollar Reserve Impact:

Trade deficits, necessary for maintaining the Dollar’s reserve status, grew from a net surplus in 1968 to $450 billion by 2000, absorbing 30 million tons of annual steel imports by 1998 (Eichengreen, 2008). By 2024, this had grown to $918.4 billion total deficit. This prioritization of imports, driven by “free trade” policies, allowed subsidized foreign steel to undercut domestic producers, violating Ricardo’s free-market assumption.

Thus, Ricardo’s theory fails to account for the artificial cost advantages created by foreign subsidies and U.S. regulatory burdens, as well as the structural trade imbalances required by the Dollar’s reserve status, as per the Triffin dilemma. Neither Japan nor South Korea nor China are inherently better suited to produce steel from a natural resources, industrial, labor pool, capital, technology, or infrastructure basis. Pennsylvania should have naturally been able to compete handily with foreign steel producers absent government and central bank interventions.

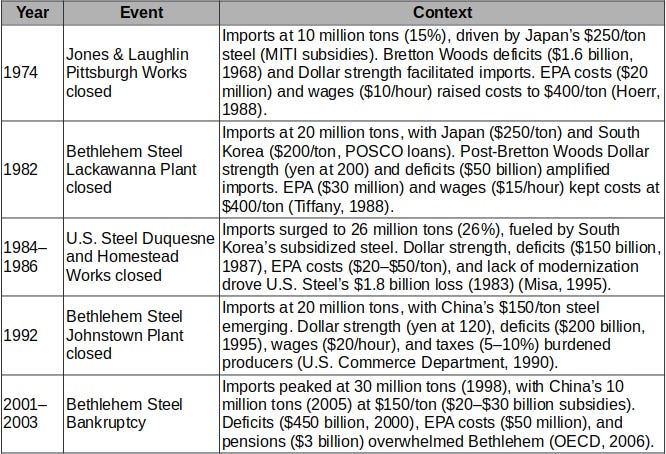

Timeline of Pennsylvania Steel Closures

Pennsylvania’s steel industry, once employing 200,000 workers in 1970, saw its workforce shrink to just 10,000 by 2005, reflecting the impact of these distortions:

These closures illustrate how the structural need for trade deficits, driven by the Dollar’s reserve status, as well as government interventions exacerbated import competition and undermined domestic steel production, leading to the dramatic decline of domestic industrial capacity, resulting in massive job layoffs, and turning Pennsylvania into a “Rust Belt” state.

Trump’s Tariffs: Countering Distortions

President Trump’s tariff policies aim to address these imbalances by reducing trade deficits and protecting domestic industries. The 2018 Section 232 tariffs (25% on steel) increased U.S. steel production by 5% to 80 million tons and added 12,000 jobs, demonstrating their potential to counteract import-driven distortions (USGS, 2020). In 2025, President Trump implemented a 10% baseline tariff on most U.S. trading partners, with higher, country-specific rates for 57 countries with trade deficits, and equivalent unfair trade practices, aiming to level the playing field for U.S. industries (Trump, 2025).

From the perspective of the Triffin dilemma, these tariffs represent a shift towards prioritizing domestic economic interests over global Dollar liquidity. However, they also risk reducing global supply of dollars, potentially undermining the Dollar’s reserve status over time. Critics argue that tariffs could lead to retaliatory measures, harming U.S. exports and exacerbating trade tensions (CBO, 2018). Nevertheless, proponents highlight their success in protecting key industries like steel, suggesting they are a necessary response to decades of “free trade” policies that have disadvantaged domestic manufacturers, particularly in light of the structural pressures identified by Triffin.

Conclusion

The decline of Pennsylvania’s steel industry is a stark illustration of how global economic structures can conflict with domestic industrial interests. The U.S. Dollar’s role as the global reserve currency, while conferring significant benefits to certain segments of society, has required persistent trade deficits that have disadvantaged sectors like steel. Foreign governments’ interventions have created artificial cost advantages for their producers, while U.S. policies have imposed additional burdens on domestic manufacturers. David Ricardo’s theory of comparative advantage fails to account for these distortions, as the cost structures were not naturally occurring but were instead shaped by deliberate political and monetary decisions that intentionally shifted wealth from industrial centers like Pittsburgh and Detroit to hubs of financial and political engineering like Wall Street and Washington, DC.

President Trump’s tariff policies represent an effort to correct these imbalances, though their long-term effectiveness and broader economic implications remain subjects of debate. As the global economic landscape continues to evolve, understanding these dynamics is crucial for crafting policies that balance global responsibilities with domestic economic health, national security, and anti-fragility.

Works Cited

Banquedefrance. (n.d.). End of the gold-dollar standard and switch to a floating exchange rate system. https://www.citeco.fr/10000-years-history-economics/contemporary-world/end-of-the-gold-dollar-standard-and-switch-to-a-floating-exchange-rate-system

Bloomenthal, Andrew (2025, April 7). Trade Deficit: Definition, When It Occurs, and Examples. Investopedia. https://www.investopedia.com/terms/t/trade_deficit.asp

Chandler, A. D. (1990). Scale and Scope: The Dynamics of Industrial Capitalism. Harvard University Press.

Chen, James. (2022, May 27). What Is a Reserve Currency? U.S. Dollar’s Role and History. Investopedia. https://www.investopedia.com/terms/r/reservecurrency.asp

Chen, James. (2024, July 02). Fiat Money: What It Is, How It Works, Example, Pros & Cons. Investopedia. https://www.investopedia.com/terms/f/fiatmoney.asp

Churella, A. J. (2012). The Pennsylvania Railroad, Volume 1: Building an Empire, 1846–1917. University of Pennsylvania Press.

Lahiri, Upamanyu (2023, August 22). The Future of Dollar Hegemony. Council on Foreign Relations. https://www.cfr.org/blog/future-dollar-hegemony

Eichengreen, B. (2008). Globalizing capital: A history of the international monetary system (2nd ed.). Princeton University Press.

Ghizoni, Sandra K. (2013). Nixon Ends Convertibility of U.S. Dollars to Gold and Announces Wage/Price Controls. Federal Reserve History. https://www.federalreservehistory.org/essays/gold-convertibility-ends

Hoerr, J. P. (1988). And the Wolf Finally Came: The Decline of the American Steel Industry. University of Pittsburgh Press.

Hogan, W. T. (1971). Economic History of the Iron and Steel Industry in the United States. D.C. Heath and Company.

Investopedia. (2025, April 19). Bretton Woods Agreement and the institutions it created. https://www.investopedia.com/terms/b/brettonwoodsagreement.asp

Joint Economic Committee. (2025, May 6). Trade Update. https://www.jec.senate.gov/public/index.cfm/republicans/trade-update/

Klein, M. (2001). A Call to Arms: Mobilizing America for World War II. Holt Paperbacks.

Misa, T. J. (1995). A nation of steel: The making of modern America, 1865–1925. Johns Hopkins University Press.

Organisation for Economic Co-operation and Development. (2006). OECD steel committee report on global steel industry trends. OECD.

Ricardo, D. (1817). On the Principles of Political Economy and Taxation. John Murray.

Siripurapu, A., & Berman, N. (2023, July 19). The Dollar: The World’s Reserve Currency. Council on Foreign Relations. https://www.cfr.org/backgrounder/dollar-worlds-reserve-currency

Stefanova, Zornitsa. (2025, March 25). US dollar share of global currency reserves in 2025. Best Brokers. https://www.bestbrokers.com/forex-trading/us-dollar-share-of-global-currency-reserves/

Tiffany, P. A. (1988). The decline of American steel: How management, labor, and government went wrong. Oxford University Press.

Triffin, R. (1960). Gold and the Dollar crisis: The future of convertibility. Yale University Press.

Trump, D. J. (2025, April 2). Executive Order Regulating Imports with a Reciprocal Tariff to Rectify Trade Practices that Contribute to Large and Persistent Annual United States Goods Trade Deficits. The White House. https://www.whitehouse.gov/presidential-actions/2025/04/regulating-imports-with-a-reciprocal-tariff-to-rectify-trade-practices-that-contribute-to-large-and-persistent-annual-united-states-goods-trade-deficits/

U.S. Commerce Department. (1990). Steel industry trade data: Imports and exports, 1960–1990. U.S. Government Printing Office.

U.S. Geological Survey. (2020). Mineral commodity summaries 2020: Iron and steel. https://pubs.usgs.gov/periodicals/mcs2020/mcs2020.pdf

Warren, K. (2001). Big Steel: The First Century of the United States Steel Corporation, 1901–2001. University of Pittsburgh Press.

Richter, Wolf. (2025, March 31). Status of US Dollar as global reserve currency: Central banks diversify into other currencies and gold. Wolf Street. https://wolfstreet.com/2025/03/31/status-of-us-dollar-as-global-reserve-currency-central-banks-diversify-into-other-currencies-and-gold/

United States International Trade Commission (USITC). (2010, October 15). Press Release: Certain Seamless Carbon and Alloy Steel Standard, Line, and Pressure Pipe from China Threatens U.S. Industry. https://www.usitc.gov/press_room/news_release/2010/er1015hh1.htm